_edited_edited_.png)

Is Roth IRA Conversion Right for You?

- Garrett Imeson, CFP®

- Jun 3

- 14 min read

Yes, a Roth IRA conversion is right for you if paying taxes now leads to lower lifetime tax liability, especially when you expect to enter a higher tax bracket in the future and have sufficient non-retirement funds to cover the tax cost. This approach is more effective during low-income years, early retirement phases, or before required minimum distributions begin, allowing conversions at favorable rates while supporting long-term tax-free growth and a more stable retirement income stream. It is also evaluated based on Roth conversion rules and how shifting funds from a traditional IRA affects both current taxable income and future tax exposure.

The decision depends on how well the Roth IRA conversion fits within your broader financial strategy, including tax diversification, income timing, and investment horizon. A Roth IRA reduces future required distributions and allows flexible withdrawals across accounts, such as traditional IRAs, Roth IRAs, and brokerage accounts. At the same time, increased taxable income, potential bracket changes, and impacts on credits or Medicare premiums must be considered, making timing and phased conversions critical for overall effectiveness.

Why Should You Consider a Roth IRA Conversion?

You should consider a Roth IRA conversion for its ability to provide tax-free withdrawals in retirement, eliminate required minimum distributions, support tax diversification, and offer greater control over future taxable income. These benefits help reduce lifetime tax exposure and improve retirement income flexibility, making it a commonly used strategy within broader Roth conversion tax planning to manage future tax brackets and reduce taxable income in retirement.

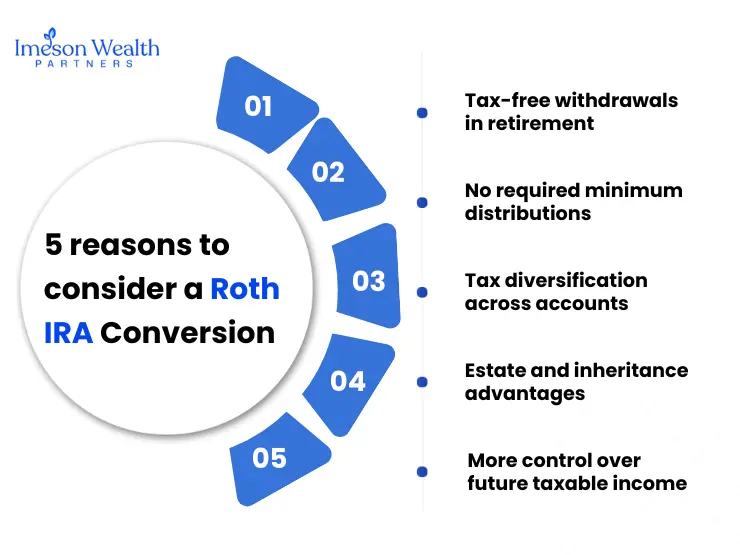

5 reasons to consider a Roth IRA Conversion are:

Tax-free withdrawals in retirement

No required minimum distributions

Tax diversification across accounts

Estate and inheritance advantages

More control over future taxable income

Tax-free withdrawals in retirement

Converting a traditional IRA to a Roth IRA allows qualified withdrawals to be entirely tax-free in retirement, with taxes paid upfront during the conversion so that both contributions and earnings can grow without additional tax liability once eligibility rules are met. This creates a predictable income stream immune to rising tax rates and eliminates Required Minimum Distributions (RMDs), which is a key part of how a Roth IRA works. To make the most of this benefit, you should meet the five-year rule for conversions and reach age 59½ before withdrawing earnings.

No required minimum distributions

Unlike traditional retirement accounts, Roth IRAs do not require minimum distributions during the account holder’s lifetime, allowing investments to continue growing tax-free for a longer period and increasing overall portfolio value. It also provides flexibility to withdraw funds only when needed, rather than on a fixed schedule. This control supports better income planning, reduces unnecessary taxable events compared to traditional IRAs, and allows retirees to preserve assets for later use or pass them on to beneficiaries efficiently.

Tax diversification across accounts

A Roth IRA conversion improves tax diversification by shifting part of your retirement savings into a tax-free account. It creates a balanced mix of pre-tax, Roth, and taxable brokerage assets, giving greater flexibility in retirement withdrawals. This strategy is often used in the conversion of traditional to Roth IRA planning to reduce exposure to higher future tax brackets and improve withdrawal efficiency.

Estate and inheritance advantages

Another key benefit of a Roth IRA conversion is improved estate planning efficiency through tax-free wealth transfer. By paying taxes at conversion, the account holder enables beneficiaries to inherit a Roth IRA that can continue to grow tax-free. Withdrawals remain tax-free when distribution rules are met, helping preserve the asset's full value. This approach lowers the tax burden on heirs while preserving more retirement wealth across generations.

More control over future taxable income

Conversion of a traditional IRA to a Roth IRA gives the taxpayer greater control over future taxable income by shifting taxation to the current year. The investor can convert funds during periods of lower income to remain within a favorable tax bracket. This approach reduces future required distributions and limits taxable income during retirement years. It also supports strategic tax planning by allowing the taxpayer to manage how and when retirement funds are taxed across different phases of their finances.

When Does Roth Conversion Make Strategic Sense?

A Roth IRA conversion makes strategic sense when you can pay taxes on the converted amount at a lower rate than you expect to face in retirement, helping reduce overall lifetime tax liability. It is particularly effective during “trough years” after retirement but before Required Minimum Distributions begin, when taxable income is typically lower. It also becomes advantageous when future tax rates are expected to rise or when decreasing RMD exposure is a priority. The strategy works well when timing, income level, and long-term retirement goals are aligned, with sufficient liquidity available to cover the tax obligation.

Does converting to a Roth IRA make sense in a low tax bracket year?

Yes, a Roth IRA conversion is suitable during a low-tax-bracket year because the taxpayer can convert a larger portion of a traditional IRA at a lower marginal tax rate. This reduces the total tax cost on the converted amount and increases the portion of retirement savings that will grow tax-free. This situation often occurs during income dips, such as job transitions or early retirement years.

Should you convert to a Roth IRA before retirement or after retirement?

A Roth conversion before retirement is more suitable when you still have earned income but expect higher taxes later, allowing you to convert funds at relatively lower current rates. After retirement, a Roth conversion is often more effective during income gap years, when taxable income temporarily declines before Social Security benefits and required minimum distributions begin. In both situations, the outcome depends on how efficiently the taxpayer aligns conversion income with a favorable tax bracket.

Does a Roth conversion help if you expect higher taxes later?

Yes, a Roth conversion becomes beneficial when the taxpayer expects to enter a higher tax bracket in the future due to required minimum distributions, retirement benefits, or tax law changes. Paying taxes at a lower current rate allows the investor to avoid higher future tax liability and preserve tax-free retirement withdrawals. Over time, growth in a Roth IRA allows both contributions and earnings to compound without being reduced by future taxation.

Is a Roth conversion useful during income gap years?

Yes, income gap years create an ideal conversion window because the taxpayer can convert retirement funds while taxable income remains low. This allows the investor to fill lower tax brackets efficiently without triggering higher marginal rates. This strategy reduces long-term tax exposure and prepares the retirement account for tax-free growth before required distributions begin.

When a Roth IRA Conversion Might Not Be Worth It?

A Roth conversion may not be worth it when the upfront tax cost outweighs the long-term benefit, particularly if there is no outside cash available to cover the tax bill, the investor expects a lower tax bracket in retirement, or the investment horizon is too short to recover the cost. It can also be disadvantageous if it pushes income into a higher tax bracket or increases Medicare premiums through IRMAA, adding unnecessary near-term financial burden without sufficient long-term tax advantage.

Does a Roth conversion increase your current tax burden too much?

Yes, a Roth conversion can significantly increase your taxable income in the year of conversion because the converted amount is treated as ordinary income. This can push the taxpayer into a higher tax bracket and significantly increase the total tax liability. If the conversion moves income into higher brackets, such as 32% or above, the upfront tax cost may reduce the overall benefit of tax-free growth. This situation becomes less efficient when the taxpayer cannot offset the tax impact through strategic planning.

Should you avoid conversion if you need the money soon?

Yes, you should avoid a Roth conversion if you need the money within five years. Converting triggers an immediate income tax bill, and withdrawing within five years can trigger penalties, meaning you could lose money overall. This conversion strategy is not suitable for short-term use because it relies on long-term tax-free growth to offset the upfront cost. Early withdrawals reduce the benefits of compounding and may violate the five-year rule or the age 59½ requirement, resulting in additional taxes and penalties.

Does a Roth conversion impact tax credits or benefits?

Yes, a Roth conversion significantly impacts tax credits and benefits because the converted amount is treated as taxable income in the year of the conversion, increasing your Adjusted Gross Income (AGI). This higher income level can reduce eligibility for income-based tax credits and deductions, such as the Child Tax Credit, and may also trigger higher Medicare premiums through IRMAA thresholds. These indirect costs can increase the overall expense of the conversion and reduce its net financial advantage, making careful tax planning essential to assess whether the long-term benefits still outweigh the short-term impact.

Who Benefits Most from Roth Conversions?

High-income earners, early retirees, young investors, and individuals with multiple IRAs benefit most from Roth conversions. This strategy is most effective for those positioned to pay taxes at lower current rates while locking in tax-free retirement withdrawals and greater control over the timing of future income, especially if they expect higher tax exposure later.

High-income earners

Converting a traditional IRA to a Roth IRA offers high-income individuals a strategic way to reduce future Required Minimum Distribution exposure by shifting retirement savings into a tax-free account. This is particularly beneficial for those with substantial balances that could result in large taxable distributions later in retirement. It also serves as a tax rate management strategy, allowing investors to spread conversions over multiple years to avoid higher marginal tax brackets and increase tax-free withdrawals.

Early retirees

A Roth IRA conversion becomes particularly effective for early retirees because their taxable income often drops after they stop working. This lower-income phase creates an opportunity to convert traditional IRA funds at lower tax rates than would be paid on higher-income sources. During this period, the retiree can use lower tax brackets to shift assets into a Roth account, supporting long-term tax-free growth and improving future income flexibility.

Young investors

Young investors benefit most from Roth conversions as they have a long time horizon for tax-free compounding. Converting early means paying taxes on a smaller balance while locking in decades of future growth inside a tax-free Roth account. Over time, this can significantly increase retirement wealth since all investment gains remain sheltered from future taxation. It also provides flexibility later in life, as withdrawals can be made tax-free without worrying about future tax rate increases or Required Minimum Distributions.

Investors with multiple IRAs

Investors who hold retirement savings across multiple IRA accounts and other retirement plans can benefit from greater control over the timing of conversions. This flexibility allows specific accounts or partial balances to be selected for Roth conversion, which enables precise management of taxable income within a given year. Holding multiple Roth IRAs also supports coordination with brokerage accounts, enhancing tax diversification and helping maintain stable retirement income amid changing tax conditions.

What types of accounts can you convert to a Roth IRA?

The main account types eligible for a Roth IRA conversion include Traditional IRA, 401(k), 403(b), SEP IRA, and SIMPLE IRA, each allowing investors to convert retirement funds via a transfer or rollover with varying conversion rules, taxes, and eligibility limits. Understanding the differences among the various types of Roth IRA accounts helps you choose the most tax-efficient conversion path and avoid unexpected tax consequences during the rollover process.

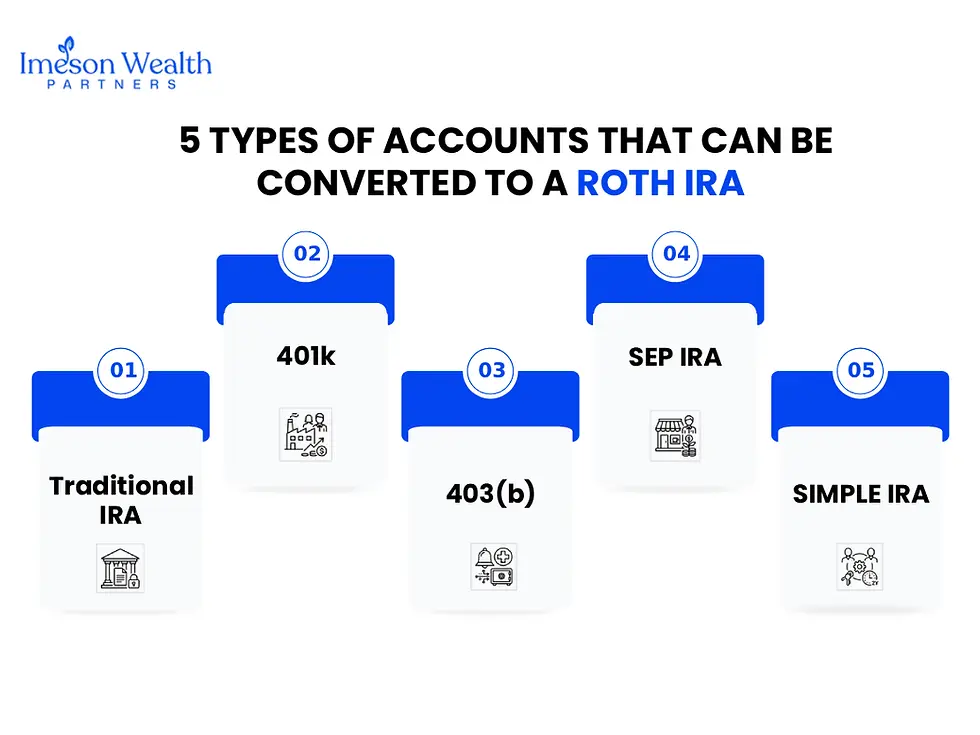

5 types of accounts that can be converted to a Roth IRA are:

Traditional IRA

401(k)

403(b)

SEP IRA

SIMPLE IRA

Traditional IRA

A Traditional IRA is a pre-tax, tax-deferred retirement account in which earnings grow until they are withdrawn. It is commonly used for Roth IRA conversions by transferring funds from a Traditional IRA to a Roth IRA. The converted amount is treated as taxable income in the year of conversion. A key limitation is that required minimum distributions must begin at age 73 if the account is not converted.

401k

A 401(k) is an employer-sponsored retirement plan funded with pre-tax contributions and tax-deferred growth. It can be converted to a Roth IRA through a rollover after leaving the employer or via an in-plan conversion. The converted balance is taxed as ordinary income. However, plan rules may limit or prohibit in-service conversions, and such conversions can increase the tax burden in the year they are made.

403(b)

A 403(b) is a tax-deferred retirement account for public sector and nonprofit employees. Funds can be converted to a Roth IRA through a direct rollover IRA. The converted amount is treated as taxable income in the year of conversion. In many cases, the ability to convert is constrained because funds cannot be accessed until separation from the employer.

SEP IRA

A SEP IRA serves self-employed individuals and small business owners through pre-tax employer contributions that grow tax-deferred. The account can be converted to a Roth IRA by transferring funds and recognizing the converted amount as taxable income. Large balances can increase the tax on Roth conversion, which requires careful bracket planning.

SIMPLE IRA

A SIMPLE IRA is a pre-tax retirement plan for small business employees and employers. It can only be converted to a Roth IRA after a two-year holding period, following Roth conversion rules. The converted amount becomes taxable income. This restriction limits early conversion and affects timing within a broader Roth conversion strategy.

How Are Roth IRA Conversions Taxed?

A Roth IRA conversion is taxed as ordinary income in the year of conversion, with the pre-tax amount added to taxable income, which may increase your tax bracket or affect deductions and credits. The total tax impact depends on conversion timing, income level, and strategy, as taxpayers can reduce liability by spreading conversions over multiple years or by using low-income years. This makes timing and income planning important when deciding how much to convert within a given tax bracket.

Does a Roth conversion count as taxable income?

Yes, a Roth conversion transfers funds from a traditional IRA to a Roth IRA and triggers ordinary income tax on the pre-tax amount in the year of conversion. The converted amount is added to taxable income, which can move the taxpayer into a higher tax bracket and affect deductions or credits. There are no income limits on Roth conversions, which makes tax planning essential.

Can you reduce taxes on a Roth conversion?

Yes, you can reduce taxes on a Roth conversion by timing it during low-income years, spreading it over multiple years to avoid higher tax brackets, and converting during market downturns to lower the taxable amount. This approach helps manage your overall tax liability and improves long-term tax efficiency.

Should you pay Roth conversion taxes from outside funds?

Yes, paying Roth conversion taxes with outside funds such as cash or brokerage accounts keeps the full converted amount invested in the Roth IRA, supporting tax-free compounding. Using retirement funds reduces the balance available for growth and may trigger early withdrawal penalties if the taxpayer is under age 59½, lowering overall benefits.

How Much Should You Convert to a Roth IRA?

The right amount for a Roth IRA conversion is determined by converting only enough income to stay within your current tax bracket while increasing tax-free growth. A Roth conversion calculator can help estimate tax on Roth conversion and identify how much you can convert without moving into a higher tax bracket. This approach works well during low-income years, such as early retirement before required distributions begin, which improves long-term tax efficiency.

How do you find the right amount to convert without moving into a higher bracket?

You can determine the optimal Roth IRA conversion amount by calculating your current taxable income and identifying the remaining space within your target tax bracket. This involves subtracting projected taxable income from the top threshold of the bracket to find how much you can convert without moving into a higher rate, which helps control tax liability while increasing tax-free retirement savings.

Should you convert all at once or in phases?

You should follow a phased Roth IRA conversion strategy, which is more effective than a lump-sum conversion. Phased conversion spreads taxable income across multiple years, decreasing bracket creep and reducing the risk of being pushed into a higher tax bracket. This approach helps the taxpayer avoid higher rates, maintain eligibility for deductions, and align conversions with favorable income periods.

How does partial conversion reduce tax impact?

A partial Roth IRA conversion reduces the tax impact by limiting the amount added to taxable income in a single year and allowing the taxpayer to move funds gradually rather than triggering a large, one-time tax bill. This strategy spreads tax liability across multiple years, helps avoid bracket creep, and keeps income within lower tax brackets while preserving eligibility for credits or deductions.

What Are the Risks of Roth IRA Conversion?

The primary risks of a Roth IRA conversion include immediate tax liability, incorrect timing of the conversion, impact on Medicare premiums, and market timing risk. A conversion increases taxable income, which may push you into a higher tax bracket and reduce credits or subsidies. Poor timing can lead to unnecessary taxes, while higher income may trigger IRMAA and raise Medicare costs. Converting at high market values can also mean paying taxes on assets that later decline in value.

Immediate tax liability

A Roth IRA conversion creates immediate tax liability because the converted amount is taxed as ordinary income in the year of conversion, which can raise taxable income, push the taxpayer into higher tax brackets, and increase Medicare premiums under IRMAA. The upfront tax burden can reduce cash flow, and using IRA funds to pay taxes may lower retirement savings and trigger a 10% penalty if the taxpayer is under age 59½.

Incorrect timing of conversion

The timing of a Roth IRA conversion directly affects tax efficiency and long-term outcomes, as converting during high-income years can push the taxpayer into a higher bracket and increase tax liability. Incorrect timing may also reduce ACA subsidies, ignore 5-year rules, or fail to spread conversions. Market downturns after conversion can further reduce the account's value, even after taxes have already been paid.

Impact on Medicare premiums

A Roth IRA conversion requires paying income tax on pre-tax funds at the time of conversion, which can increase overall income and push the taxpayer into higher tax brackets. This rise in income may also trigger IRMAA adjustments, leading to higher Medicare Part B and Part D premiums. If these additional costs are not planned for, they can reduce the long-term financial advantage of the conversion strategy.

Market timing risk

Market conditions at the time of a Roth IRA conversion can affect outcomes, as converting at high asset values increases the taxable amount while a later decline reduces account value after taxes are paid. This risk is irreversible. A Roth IRA conversion also carries a large upfront tax bill, may push the taxpayer into higher brackets, increase Medicare premiums through IRMAA, and reduce eligibility for tax credits or financial aid.

What Rules Should You Know Before a Roth IRA Conversion?

The key Roth IRA conversion rules include the 5-year rule, pro-rata rule, and conversion limits that affect how funds are taxed and accessed. These rules determine eligibility, taxation, and withdrawal timing. There are no income limits on conversions, but the converted amount is taxed as ordinary income in the year it is completed. Employer plan rollover rules may also apply to accounts such as 401(k)s, making timing and account structure important for efficient planning.

What is the 5-year rule for Roth IRA conversions?

The Roth IRA conversion 5-year rule requires that each conversion of pre-tax funds must remain in the account for at least five years to avoid a 10% penalty if the taxpayer is under age 59½. The five-year period starts on January 1 of the conversion year, and each conversion has its own timeline, which affects withdrawal planning and tax treatment.

What is the pro-rata rule in Roth conversions?

The pro-rata rule (or proportional rule) is an IRS regulation requiring that Roth conversions be taxed based on the ratio of pre-tax to after-tax money across all traditional, SEP, and SIMPLE IRAs. The IRS uses total IRA balances to determine the taxable portion, which prevents isolating and converting only after-tax contributions to avoid taxation.

Are there limits on Roth IRA conversions?

There are no IRS income limits or dollar limits on Roth IRA conversions, allowing taxpayers to convert any amount from eligible retirement accounts. However, the converted amount is fully taxable as income, so the practical limit depends on the taxpayer’s ability to manage tax liability within a target tax bracket.

Can you do multiple Roth conversions in a year?

Yes, you can complete multiple Roth IRA conversions within the same year, which provides flexibility in managing taxable income. This approach allows adjustments in response to income changes, tax-planning needs, or market conditions, helping to optimize the overall conversion strategy.

Can You Convert a 401(k) to a Roth IRA?

Yes, you can transfer a 401(k) into a Roth IRA through a process known as a Roth conversion, which shifts pre-tax retirement funds into an account that allows tax-free growth and qualified withdrawals in the future. This strategy can improve long-term tax efficiency when aligned with your income and retirement planning goals.

However, the converted amount is treated as ordinary income in the year of transfer, which may increase your tax liability and affect your tax bracket. This option is typically available after leaving an employer or through in-service withdrawals if permitted.

How Do You Know if a Roth IRA Conversion Is Right for Your Situation?

A Roth IRA conversion is generally suitable when you expect to be in a higher tax bracket in the future, have sufficient non-retirement funds to cover the tax liability, and can benefit from long-term tax-free growth. It becomes more effective when aligned with favorable tax conditions and long-term retirement goals.

You should also evaluate factors such as low-income years, upcoming required minimum distributions, and tax diversification needs. A well-timed Roth conversion can increase tax-free income, reduce future taxable distributions, and provide greater control over retirement cash flow. These considerations are an important part of retirement income planning, as they help align tax strategy with long-term income needs, withdrawal timing, and overall financial stability in retirement.

Comments